We’ve just got back from Nuremberg, where BIOFACH 2026 brought together the global organic community under the theme “Growing Tomorrow: Young Voices, Bold Visions.”

This year was special for us because it was our first time exhibiting with our own booth.

Over four days, we met with long-term partners, new buyers, processors, policymakers, certification bodies, and innovators. The latest BIOFACH 2026 organic trends show certain shifts in the sustainable food industry. Here’s what stood out, and what it means for the organic sector.

BIOFACH 2026 organic market trends show the market is growing, but its structure needs strengthening

Each year, FiBL shares the latest statistics on organic agriculture. Once again, the numbers confirmed something encouraging: organic demand continues to grow.

Globally, the organic market reached €145 billion in retail sales in 2024. The United States is still the largest consumer market, with imports continuing to rise. Australia has the most organic farmland, India has the most producers, and Mexico is the top exporter, particularly to the US, predominantly of bananas, followed by oils and fats.

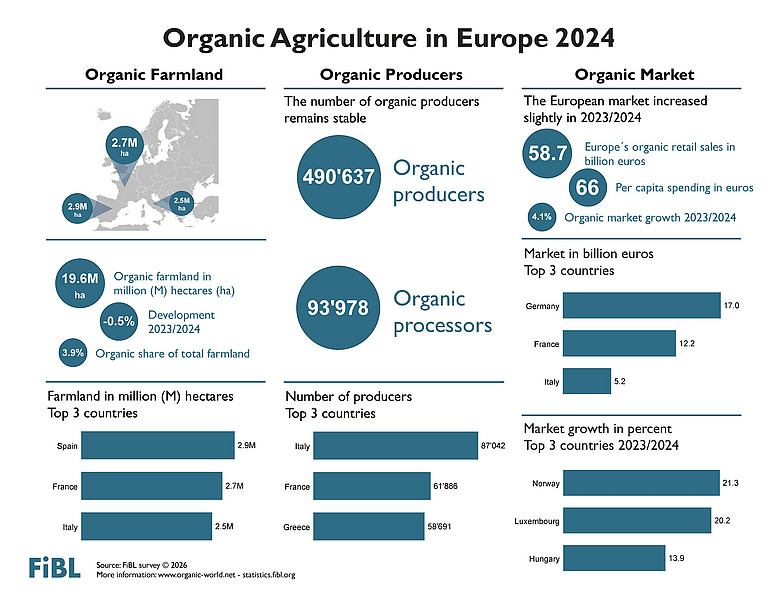

Europe shows a similar trend. According to FiBL’s latest report, the European organic retail market reached €58,7 billion, growing by 4,1% in 2023/2024. Germany is still the largest market at €17 billion, followed by France (€12,2 billion) and Italy (€5,2 billion). Average per capita spending across Europe stands at around €66.

At the same time, Europe has 19,6 million hectares of organic farmland, which is 3,9% of all agricultural land. This area dropped slightly by 0,5% from 2023, while the number of organic producers, about 490.000, stayed about the same.

Looking more closely at the structure of that land, the 19,6 million hectares are almost evenly split for the first time. Grazing fields account for 8,4 million hectares, and arable land also covers 8,4 million hectares. Permanent crops make up the remaining 2,4 million hectares.

In short, demand in the EU is rising faster than the number of producers.

This imbalance matters. It raises questions about resilience and long-term supply security. Many of our conversations circled back to this. When the number of producers doesn’t keep up with demand, reliability stands out. Buyers want more than just organic certifications. They’re looking for partners who can demonstrate consistent yields, traceability, food-grade quality, and the ability to deliver year after year.

That’s one more reason we’re sharing our harvest data openly. If you want to see how our crops performed in 2025, including quality parameters relevant for food-grade production, you can explore our full results below.

Organic regulation aims to protect trust while simplifying compliance

But stability in organic farming doesn’t depend only on farms. It also relies on the rules and regulations that shape how the sector works.

Luis Carazo Jimenez, Head of Unit “Organics” at DG AGRI (European Commission), made the priority clear: protect the EU market and consumers with real, unquestionable organic products.

The Commission is working on a 10-year supportive framework designed to stimulate organic production, and there is clear recognition that organic production is currently complex and that regulation adds another layer of complexity. Simplification is being explored, but not at the expense of consumer protection.

The goal is to have regulatory changes in place by the end of 2026. And importantly, the Commission invited stakeholders to contribute proposals based on practical experience.

Michael Reynaud (Vice President, Ecocert) reinforced that strict regulation is necessary if consumer trust is to remain intact. At the same time, regulation must function as support for producers, not just control. Tomas Fertl (BIO Austria & IFOAM Organics Europe Board member) voiced what many stakeholders experience daily: the framework can be overly complicated and difficult to implement in practice. Some obligations are not consistently applied, which weakens coherence.

The discussion that followed made it clear that the organic sector isn’t against regulation. Instead, it wants clearer and more practical rules.

For us, this confirmed what we already believe: digital tools and transparency are key for compliance, consistency, and long-term resilience.

Plant-based organic trends at BIOFACH 2026

Another lecture that stood out was from IFOAM Organics Europe, which connected organic farming and food directly to plant-based policy and market growth.

The European plant-based market is currently valued at around €10 billion and is projected to double by 2030.

But one insight stood out: plant-based growth doesn’t automatically mean organic growth. Many plant-based producers are not rooted in organic farming. The session highlighted growing EU-level collaboration toward a Plant-Based Action Plan, alongside examples, such as Denmark, where policy and state-supported food programs more intentionally link plant-based strategies with organic production.

At the same time, consumer preferences are shifting. They are no longer primarily searching for meat substitutes. They are moving toward simpler, cleaner, less processed foods—fewer, familiar ingredients, and clean labels. There’s also growing interest in functional grains, legumes, and minimally processed organic ingredients intended for direct human consumption.

This shift toward simplicity is something we’re genuinely glad to see, and are actively building toward with Niamito. We had thoughtful discussions with potential distribution partners who see the same direction emerging in their markets: demand for clean-label, nutritionally meaningful, organic convenience.

Plant-based growth continues, and brands that focus on authenticity and good nutrition may benefit most.

Launching The Origin Marketplace

During these strategic discussions, one practical frustration kept appearing on both sides of the supply chain.

Farmers struggle to find reliable buyers, and buyers struggle to find reliable, transparent suppliers.

That’s why we chose BIOFACH 2026 to launch The Origin Marketplace.

The idea is straightforward and simple: a multilingual, open platform where farmers can list what they grow and buyers can explore availability, certificates, and origin transparently.

The feedback was encouraging, particularly among farmers looking for additional sales channels and buyers seeking a stable European organic supply and more direct communication channels. It’s now clear that digital tools are no longer a “nice addition.” They’re becoming core to how organic trade functions.

BIOFACH 2026 from our booth

This year’s Biofach was different for us. It was our first time exhibiting with our own booth.

At our stand, visitors saw real crops from our fields—peas, oats, wheat, chickpeas, flax, and sunflowers. Each had an Origin QR code that, when scanned, revealed the process from sowing to harvest and storage.

We reconnected with long-term partners and met many new people who are advancing sustainable farming and food.

BIOFACH 2026 confirmed that organic is no longer defined by being alternative. It’s now part of the core market structure, and market growth needs strong foundations. Plant-based growth should stay true to organic principles, simple ingredients, transparency, and integrity, while digital tools and direct sourcing reduce complexity in the supply chain.

From our point of view, the way forward is clear:the farms and companies that succeed will be those that combine organic principles with operational strength—stable yields, traceability, digital tools, and market access.

We’re happy to already be part of that effort.