When we stroll down the aisles of our local supermarket or browse through online grocery stores, it’s easy to overlook the web of costs that make up the price of the food items we purchase. Recently, during a meeting with one of our partners, we were reminded of this fact when they pointed out that oftentimes for conventional products packaging can cost more than the actual ingredients. This realization prompted us to delve deeper into the price structures of various food products, including our own innovative, healthy, and convenient, Njamito. Are we as consumers primarily buying the raw materials we consume, or is there more to it than meets the eye?

Breaking Down the Price of Oat Flakes

Now, let’s shift our focus to oat flakes as a case study to understand what we truly pay for when we buy food. Below is a breakdown simulation (based on our research) of the cost components for a typical box of organic oat flakes priced at €2.69 in a supermarket:

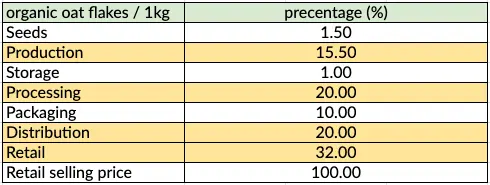

Table 1: What do we pay for when we buy oat flakes?

In examining the cost structure of a typical box of oat flakes priced at €2.69 in a supermarket, these are the various cost components contributing to the final price. They include the seed cost, accounting for a small percentage of approximately 1.5%, the significant production expenses in the field at around 15%, storage expenses at about 1%, and post-processing costs encompassing activities after harvesting and storage, which make up roughly 20%. Additionally, there are packaging costs, amounting to approximately 10%, and distribution and logistics expenses, making up 20% of the cost. Notably, the merchant’s margin, representing roughly 32% of the final price, stands out as one of the most substantial contributors. These components collectively shape the price structure of oat flakes on the supermarket shelf.

The elements highlighted in yellow in the table represent the most significant players in the final price of this product. As we can see, distribution and logistics, along with the merchant’s margin, consist of the lion’s share.

Unraveling the Price Composition of Njamito

Turning our attention to Njamito, an innovative complete meal in a bottle, we observe a slightly different cost structure. Here’s a breakdown of what comprises the €4.99 price tag for a 390g bottle.

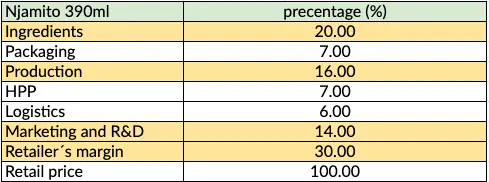

Table 2: What do we pay for when we buy Njamito?

Within Njamito’s price composition, organic raw materials constitute approximately 20% of the final price. Additionally, packaging represents about 7% of the final price.

Production expenses constitute 16% of the final price, high-Pressure Processing (HPP) – an innovative method we use for preservation – accounts for 7%, and transport and logistics contribute another 6%. A standard retailer’s margin is around 30%, which leaves us with around 14%. Some of this is invested into marketing and some into further R&D.

Once again, the highlighted segments in yellow signify the dominant price drivers. The price of production and the merchant’s cut remain substantial, reflecting the complexity of the food industry.

Interestingly enough in both cases, the price of the ingredients only amounts to about 1/5 of the final price. And we are talking about organic products here. Conventional ingredients on average cost roughly half of the price of their organic counterparts or even less in the case of highly processed industrial ingredients such as aromas that are often used to replace real fruit and vegetables. This means that with conventional products the price of ingredients can amount to only 1/10 of the final product!

The Complexity of Convenience

Why does the food industry involve so many players? The answer lies in our collective desire for convenience, daily and immediate availability. To cater to this demand, each link in the supply chain plays its own role, which comes with a price, and ultimately drives up the cost of the final product.

Our way ahead

For semi-finished products like oat flakes, an opportunity for optimisation exists to streamline our processes by setting up our own processing facilities and establishing more direct partnerships with crop buyers, which will cut down on intermediary costs.

Also, as Njamito and other products our food development team is developing are concerned, our next step for ensuring healthy food for everyone is vertical integration: using our crops as ingredients, since they are produced organically and ecologically, and more importantly we’ve established complete traceability that unveils every step we take in nurturing our crops, from seeds to storage. We are planning to introduce organic oats produced by LoginEKO into Njamito in the beginning of 2024.